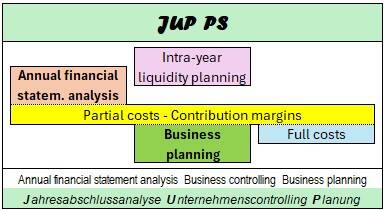

Business Planning

There are many more facets of operational planning than can be covered on this website. That is why I am referring you to my PDF, 'i Business Management: Basics, Indicators, Examples.PDF'. I promise that it covers topics that you won't find in theoretical works. This website can only spark your interest in exploring operational planning.

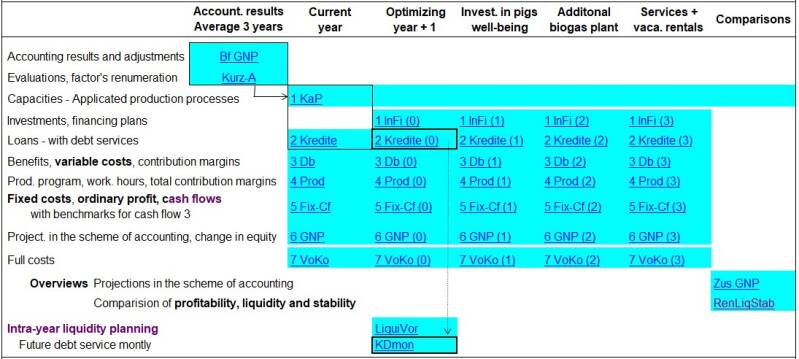

It is favourable to analyse a company already in thinking onto the business planning. This avoids any barriers between analysis and planning. For example, you can use the same loan list for the past as for the future. Therefore, the connection between analysis and planning is shown again.

Students may find the analysis challenging. However, their planning is relatively straightforward later on - because the tables are presented in the same way. At the beginning of the planning process, it should be clear what will be compared. If you want to compare alternative developments of the company, this can be expressed like this.

In this mode, you begin by calculating the current year, after which you can start exploring the alternatives. In between, you may then plan an 'optimised' variant with only a few investments.

Examples showing the target alternatives:

1. Making changes to the existing fattening pigs to improve their well-being.

2. Building an additional biogas plant on the farm.

3. Providing machinery services and holiday accommodation.

The year-after-year' scheme is often to be preferred:

This method is particularly helpful in cases of financial difficulty or when companies are facing major changes to their business model, such as the transition from conventional to ecological production in agriculture. About 50% of cases calculated by consultants working with JUP PS are using this method. The year-after-year model is similar to dynamic planning.

With JUP PS, you can switch over. When switching, the programme must make significant changes to the loan lists. This is because, in the year-on-year scheme, each loan value must be based on the previous year.

Which year should you use for the "Current Actual" column? In textbooks, you will mostly not find any proposals of departure dates. However, in real practice, this is crucial. If you are not careful enough, you will calculate the repayments a whole year or more too early. This will result in incorrect loan listings. Consequently, you will lose your reputation with entrepreneurs and bankers. You will find more on this important subject in the PDF 'i Business Management - Basics, Indicators, Examples'.

The following diagram shows that many tables can be printed out in JUP PS. But is that necessary? For example, if you will present the resultats without the Current Year and the Optimising column, you can hide them in the overviews.

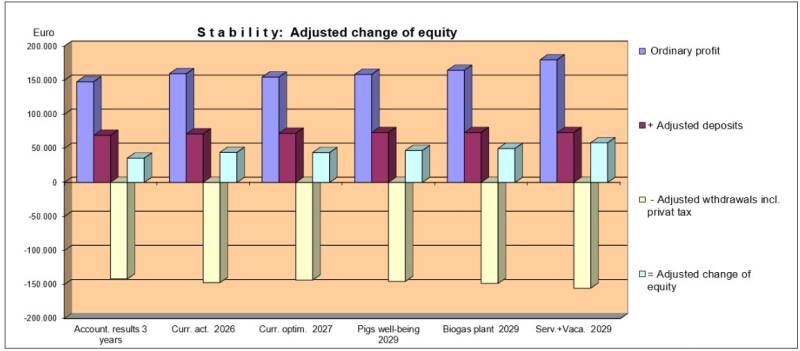

Here is a diagram on stability of a familiy company. It compares the results of accounting with the calculated profits, deposits (mainly from photovoltaic) and withdrawals, and totals up the change in equity.