Short-Term Financial Planning

If the sustainable cash flow 3 is sufficiently high — i.e. above the reinvestment level — there is no need to consider short-term debt development. However, if it is not, or if cash flow 3 is negative, the situation becomes critical. The section of intra-year planning (see page before) shows how to create a second cash flow 3 after the extraordinary cash inflows and outflows. However, a monthly intra-year planning is very time-consuming.

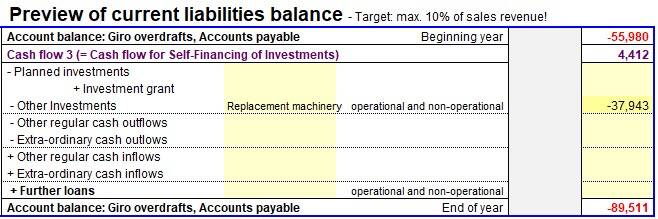

If you select the year-after-year option (in JUP PS), a special table on current liabilities balanc will open. Perhaps this table suits you.

This table begins with the short-term debts at the start of the year, to which sustainable cash flow 3 must be added. Then the planned investments must be deducted, including estimates for the unexpected replacement of machinery and equipment. Are there any cash inflows or outflows that were not included in cash flow 3? Last, the planned additional long-term loans must be taken into account. The table concludes with the short-term debts at the end of the year. Undoubtedly, entrepreneurs will find such a table easy to understand.

For more details have a look to my PDF: Business Management - Basics, Indicators, Examples.