Controlling. Costs-Benefits-Analysis. Contribution margins

The second step in assessing a company is often referred to as 'controlling'. In English, 'controlling' does mean to steer, to guide or to manage. The following is a chronological list of the key terms:

Analysis: It covers the past, including many years gone by.

Controlling: It concerns the present, the very recent past, and the very near future.

Planning: It is directed towards the future and often covers several years.

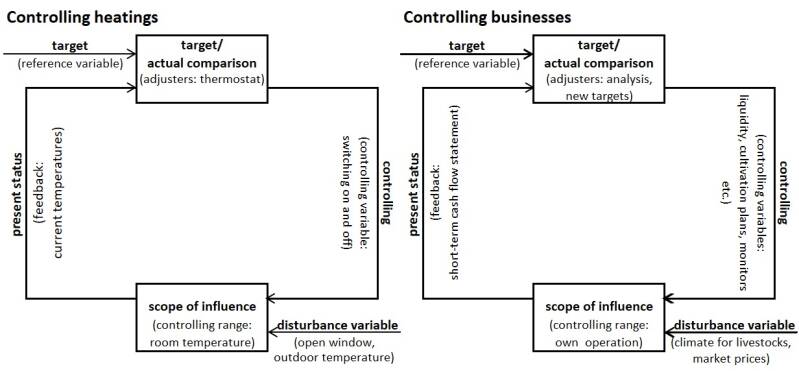

In production controlling, an increasing number of sensors can be used. There are short-term indicators. Entrepreneurs must use them. The following diagram compares heating system controlling with business controlling. In general, it is not easy to find good indicators for business controlling. In horticulture, for instance, you can compare current sales with those from the same month a year ago to adjust your advertising strategy accordingly.

The terms “benefits” and “costs” are used in reference to a company's business sectors (or production processes). Intra-company turnover between business sectors are included.

Benefits = income according to accounting records + internal turnover generated

Costs = expenses according to accounting records + internal turnover consumed

Costs can be categorised as either variable or fixed. Variable costs are proportional to the volume of production. Fixed costs include e.g., depreciation and insurance expenses. Overhead costs, e.g. interest and wage expenses, are sometimes listed separately but are often counted as fixed costs.

Formula: Contribution margin = benefits – variable costs

Device: The total contribution margin serve to cover fixed costs and generate a profit.

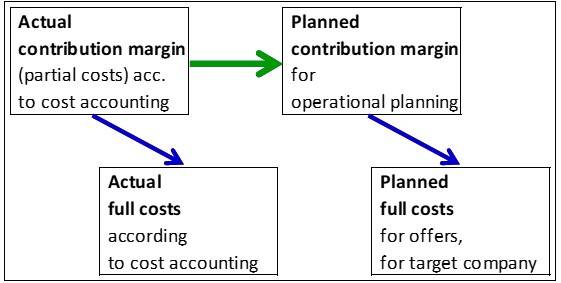

It is advantageous to calculate the contribution margin in the same way for future developments as for the analysis. This allows you to compare current and planned contribution margins. This means that you should consider cost planning before analysing past figures.

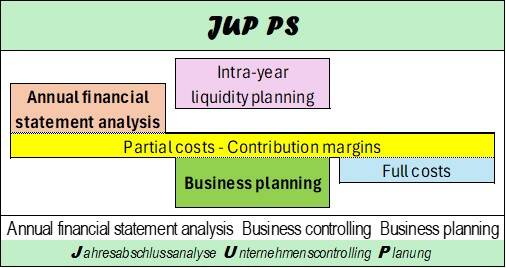

Remember the diagramme on the page 'Home'. It is taken from the JUP PS programme, which was developed by the author.

A few words on full costs, which are crucial for competitiveness. In an existing business, partial and full costs can be determined using a 'company allocation sheet'.

However, when preparing a business plan for a new company, there is nothing to allocate. Therefore, wherever possible, you should look for base numbers, for example in industry-wide company comparisons or data collections. You can then project these altogether in the form of a P&L statement.

When applying this second method to existing companies, it is often possible to obtain sufficiently accurate cost data. This is the case in agriculture, for example. If the cost of fertiliser per hectare of potatoes, etc., is known, the total fertiliser expenses for the entire farm can be extrapolated. These projections can then be compared with the expenses shown in the existing company's P&L statement.

Perhaps, this simple method of cost-benefit analysis could also be applicable in your sector of the economy. If so, it will save you a lot of time. Instead of spending several days with company's allocation sheet, you may only need to spend a few hours on extrapolations.

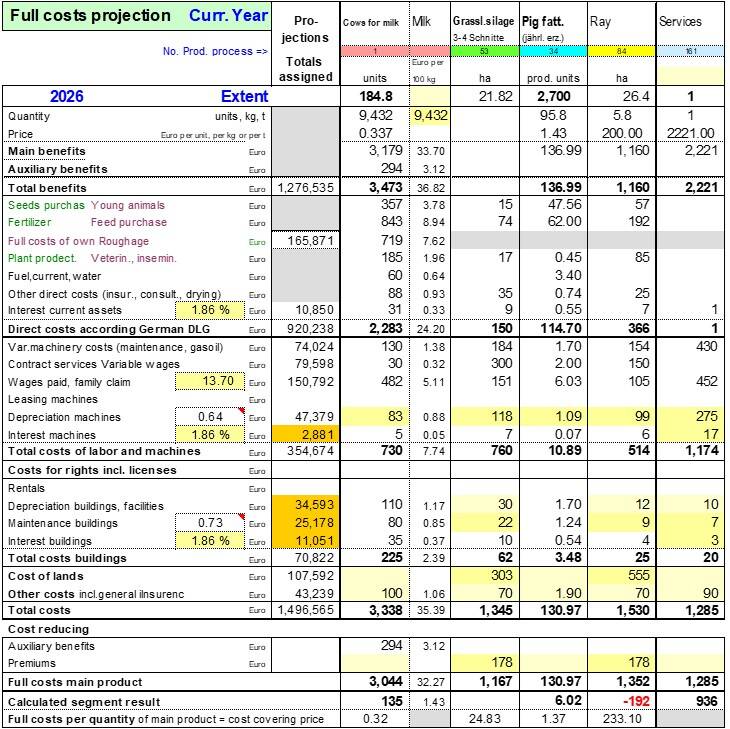

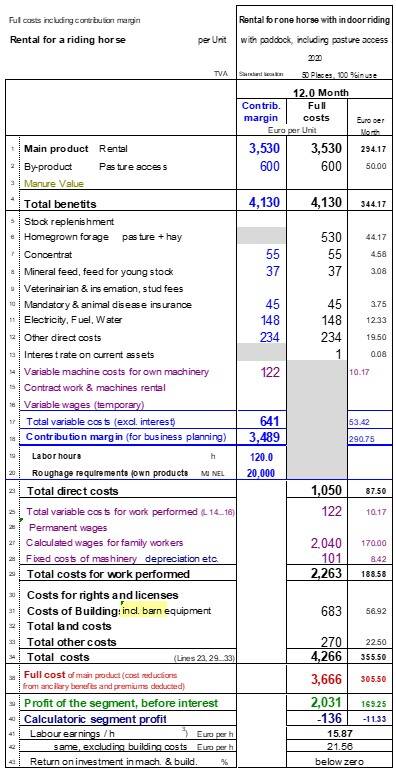

The sequence of costs often differs between cost systems. This is also the case in German agriculture, as can be seen in the following diagramme. In the contribution margin column, the variable costs of machinery appear as part of the variable costs (to be seen just before the contribution margin line). However, in the full cost column, the variable costs of machinery are included in the cost of work performed. This full-cost system was invented for a cost comparison between using in-house machinery and hiring contractors to perform field operations.

The following example shows a calculation for stable rentals for a riding horse. There, roughage is handled differently: it is shown in the contribution margin column in MJ NEL (units of nutrient required) and in the full-cost column in euros. In the case of horse rental, you will not find entries in each positions. For example, under 'veterinarian', you won't find a number. This is why such costs are paid directly by the horse's owner.

This kind of double-column system makes the different handling of costs easy to explain. It should be noted that this table with two cost columns can be used for all agricultural branches. For several years, the author converted even segment analysises into this two-columns system.

If you are interested in these subjects, see the file "i Business Management - Basics, Indicators, Examples.pdf".