Profitability. Liquidity. Stability. And about IFRS 18

Business management literature is full of advices, for example on how to start a business. A wide range of terms can be found, including 'business ideas'. However, the indicators whether the business runs or not, often take a back seat. The file 'i Business Management - Basics, Indicators, Examples.pdf' contains more informations on these subjects. You can download it (button below). This website will focus solely on period liquidity, more exactly to the cash flows. At the end of this page, it is referred to the new "standard" IFRS 18.

In short, what is the difference between profitability, liquidity, and stability?

Profitability

shows whether a business's results are better or worse than expected. It is measured by the quantity of each factor engaged: Labour and capital (in agriculture, land is an additional factor).

Liquidity

must be maintained throughout the entire period (e.g. the whole year), on a daily basis. Checking liquidity should not only be done after the annual financial statement is ready. It is an ongoing challenge.

Stability

can only be judged after the annual financial statement is ready. The most important criteria are debt coverage, the equity rate and equity growth.

For more details, see 'i Business Management - Basics, Indicators, Examples.pdf'.

Comparing 'cash flows' including 'debt service limit'

Now, let's focus on period liquidity comparing different cash flows. A good understanding of cash flows can help to avoid liquidity problems and even bankruptcy.

The 'direct method' of derivation starts from the accountants' 'Gross cash surplus'. This is easy to understand. If you look for real-time cash flow, then you must take the direct method. However, the 'indirect method' is mostly used with 'ordinary profit' as the starting point.

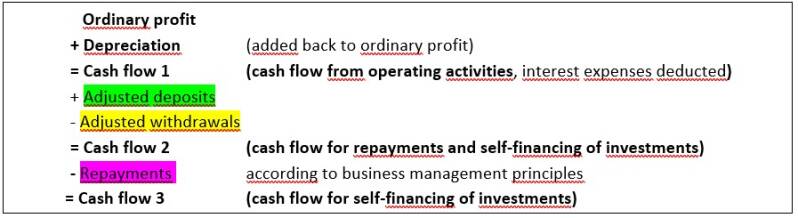

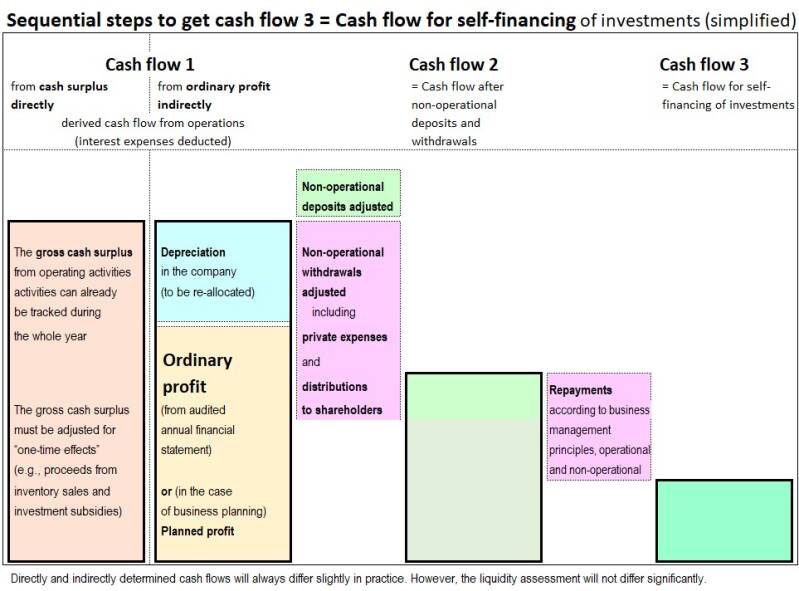

Cash flow 1, cash flow 2 and cash flow 3

Scientists have developped the 'cash flow for self-financing of investments', also known as 'cash flow 3'. This cash flow shows the 'self-financing capacity'. The staggered calculation from cash flow 1 to cash flow 3 has been teached to German agricultural students and agriculture master candidates for decades.

In order to achieve cash flow 2, it is necessary to integrate adjusted deposits and withdrawals. Withdrawals: In large groups, annual dividends limit the capacity for repayment and investment. In family companies, household costs, including nutrition, private insurance premiums, and personal tax for the whole family, must be considered. Deposits from non-company sources may include, for example, rental income or cash from photovoltaic panels. In SMEs, there are often non-company earnings that support the family.

For cash flow 3, debt repayments must be deducted.

These three cash flows are relevant for both micro-businesses and large, internationally active groups.

As known from accounting, there are four classes of accounts.

1a. Financial accounts

1b. Tangible asset accounts

2a. Income and expenses accounts (profit accounts)

2b. Private or personal accounts (deposits and withdrawals)

This means that the Cf1 to Cf3 system is the closest to accounting. However, while moving from cash flow 1 to cash flow 2, you can see the deposits and withdrawals in their adjusted form.

Useful benchmarks or metrics for cash flow 3 are reinvestments. Typically, reinvestment is equal to total depreciation (including amortisation). This is the long-term benchmark. However, a better benchmark is often depreciation of machinery (and perennial crops in agriculture), since reinvestment in buildings is usually unnecessary for at least 15 years. This is the mid-term benchmark.

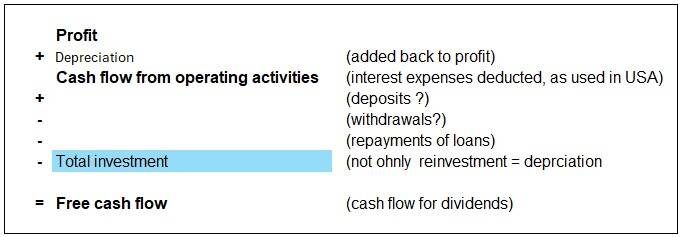

Free cash flow

It should answer to the question of how much can be paid out to shareholders in dividends. The definitions of free cash flow found in literature do not take deposits and withdrawals into account. Usually, its start with the non-adjusted profit.

Consequences:

a) If investments are minor, the company can pay huge dividends or withdrawals.

b) If investments are high, no dividends or withdrawals can be paid.

Therefore, free cash flow does not seem to be a reliable indicator.

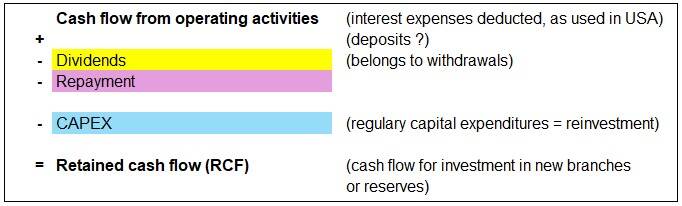

Retained cash flow

Retained cash flow is similar to the aforementioned 'cash flow for financing investment' (cash flow 3). But, the 'normal' depreciation (CAPEX) has already been deducted, whereas in the Cf3 approach, depreciation is used as a metric.

According to the definitions found: The base is profit, not ordinary profit. And as with free cash flow, only dividends appear as withdrawals.

Non-company deposits are not taken into account. But, you will also find deposits in big companies, such as from rented residential properties or photovoltaic systems, which do not belong to the analysed company. If there is no need for reinvestment in these areas, the entrepreneur can use this cash for cross-financing.

In short, the retained cash flow should show how much cash remains after the historical depreciation.

You will find advice to look at the retained cash flow for the last two years, calculate the difference between them, and then use this amount for next year. It seems that the supporters also do not respect the four classes of double-entry bookkeeping. This may explain why term deposits and withdrawals do not appear in retained cash flow formulas.

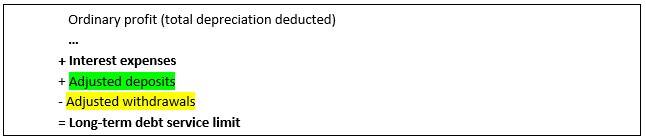

Debt service limit

In German agriculture, at least, the term 'debt service limit' is widely used.

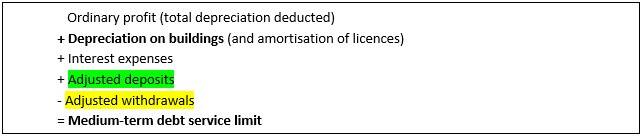

In the long-term debt service limit, the full reinvestment (i.e. total depreciation) is deducted (because ordinary profit is used as the starting point).

However, when it comes to the medium-term debt service limit, the only thing that is deducted is the depreciation of machinery (and perennial crops).

The residual value reflects long-term and medium-term cash flow 3 benchmarks.

To reduce the number of terms a practitioner has to know, both of the 'debt service limits' can be disregarded.

Let's go back to the device 'Few but meaningful terms'. The Cash Flow 1 to Cash Flow 3 scheme is the prefered. So let's take a closer look.

On what basis are the liquidity terms calculated: adjusted or unadjusted figures?

There may be a discussion about whether the starting point for the definition of cash flow should be ordinary profit or the (unadjusted) profit itself. And whether incorporated deposits and withdrawals should be adjusted or not.

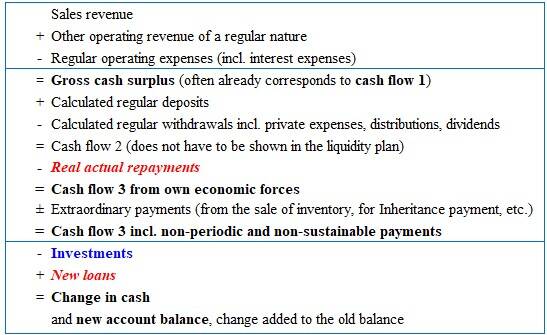

Well, the starting point for the 'debt service limit' has always been ordinary profit, adjusted deposits and withdrawals. The debt service limit should demonstrate the ability to generate sufficient funds without extraordinary cash inflows and outlows. Thus, the debt service limits showed sustainable values. The same applies to cash flows 1 to 3. They should also show sustainable values.

Liquidity in the short term

When calculating this, a different approach is required. Really, in short-term planning, extraordinary payments may have a significant impact. Thus, in an intra-year liquidity plan, cash flow 3 will be calculated twice, as shown in the following definition.

Other terms containing the words 'cash flow'

Discounted cash flow (DCF)

Although the DCF is a useful concept, it can only be used for future calculations. It involves discounting the estimated cash flows for subsequent years to their present value using financial mathematics. Therefore, DCF is not a means of analysing annual financial statements. DCF is just for planning! It shows profitability more than liquidity.

Cash flow statement

"Capital flow accounting" was already well known in the 1970s. It showed where capital came from (including new capital from loans) and where it went. It was constructed within the convention of "debit" and "credit". The totals on the left and right were equal. However, this system was not well received. Apart from accountants, it was almost forgotten. Later on, the term 'cash flow statement' emerged in the United States. Currently, the International Accounting Standards Board (IASB), an international but private association (to which the United States does not belong), has incorporated the cash flow statement into its International Financial Reporting Standards (IFRS). Note: It is not an incator of liquidity!

It is a pitty, that the accountants use also the name "cash flow". Surely there were less confusion if they would talk abaut "capital flow" - in Germany they still use "Kapitalflussrechnung". Well, the business management experts could have chosen the line on "cash surplus" because they start with the "gross cash surplus" (in direct method). At least, it is confusing to call different things with the same name.

The author researched the German BayWa Group found that the cash flow statement did not help BayWa avoid illiquidity. During this research, he came across IFRS 18, which was published in April 2024. For a more detailed discussion, see the article "i Stop the 'Three Activities' in IFRS 18.pdf".

See also the section 4.4 of "i Business Management - Basics, Indicators, Exemples.pdf".

The IASB itself emphasises improvements for investors. IFRS 18 would lead to companies being valued more accurately. That is why the author also conducted further research into how professional company valuers estimate values. It was found that some professionals use equity rate or equity growth as the basis for their evaluations. Other professional evaluators use many terms that are already familiar from analyses. However, nobody takes cash flow statements into account!

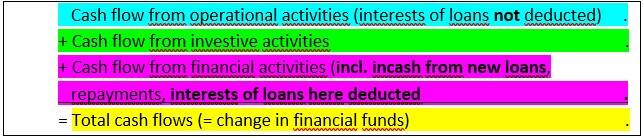

The cash flow statement is constructed with three layers, just unlike the staggered cash flows shown above. New in IFRS 18 is that interest expense on loans is no longer deducted from 'cash flow from operating activities' as before. Now, this deduction has been transferred to 'cash flow from financial activities'. This change leads to confusion. However, some groups and companies may prefer this transfer because they can legally hide poor results.

The cash flows we discussed above are all based on money made by the company itself. However, in the cash flow statement, the total cash flow statement also includes cash from new debts. This implies that all expenses were paid through a combination of own funds and new debts. In fact, this is nonsense!

As shown above, the cash flow system from cash flow 1 to cash flow 3 is the closest to accounting. See for example the deposits and withdrawals.

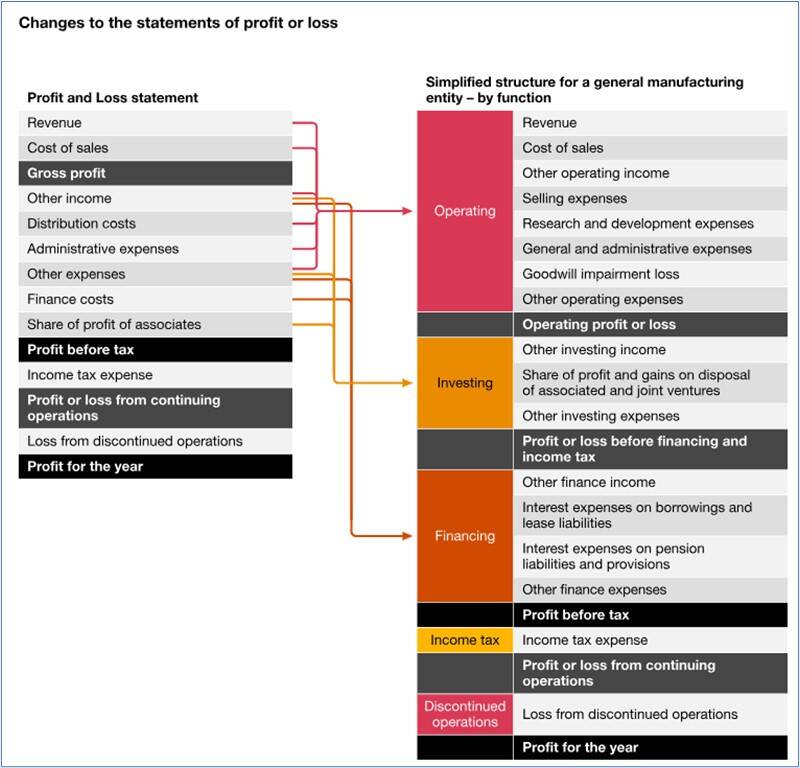

According to IFRS 18, the 'income statement' will also be categorised into 'three activities'

As an analyst, you might think that these 'activities' according IFRS 18 relate to labour remuneration. However, accountants use the term 'activity' to mean something completely different.

Similarly to the cash flow statement, interest expenses should be now transferred to 'profit/loss from financial activities'. This means that 'profit from operational activities' will automatically be higher than before.

In 2024, PwC (PricewaterhouseCoopers) published an overview of the changes to the P&L statement due to IFRS 18. PwC is one of the major auditing firms.

The income statement will change significantly. However, these changes do not benefit entrepreneurs. Similarly, investors are not better placed to judge the value of a company.

It is strange that accounting boards (such as the IASB or the FASB in the USA) refer to themselves as 'standard setters' and neglect the fundamental accounting terms 'gross cash surplus', 'deposits' and 'withdrawals' (contrary to Cf1 to Cf3).

Instead, they invent cash flow and income statements that bear no relation to accounting terms.