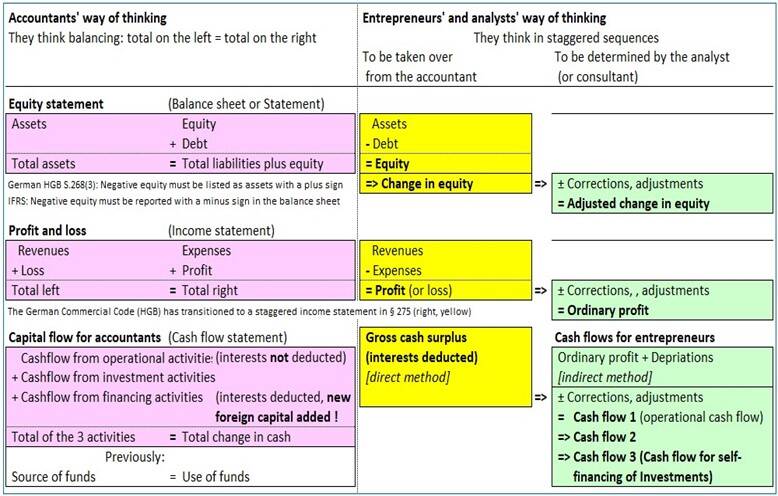

Gross cash surplus, Profit, Ordinary profit.

Assets, Debts, Equity.

Equity in an over-indebted business.

Why was this page written?

1. To demonstrate how accountants can present their annual financial statements in an easily understandable way.

2. It must be shown that analysts (or entrepreneurs themselves) can directly transfer the accountant's work into the company's financial statement from a business management viewpoint by using so-called adjustments.

3. If the company has had a bad year, it is certainly not a good idea for the tax advisor to recommend premature depreciation. The entrepreneur must be trained to make favourable decisions himself.

4. The inconsistency of the traditional accounting theory becomes obvious in cases of over-indebtedness.

5. It should be recognised that accountants and entrepreneurs think differently.

The annual financial statement always includes two sections:

- The profit and loss statement (P&L).

- The balance sheet.

For entrepreneurs, the P&L takes precedence. This order is standard in accounting for associations (at least in Germany).

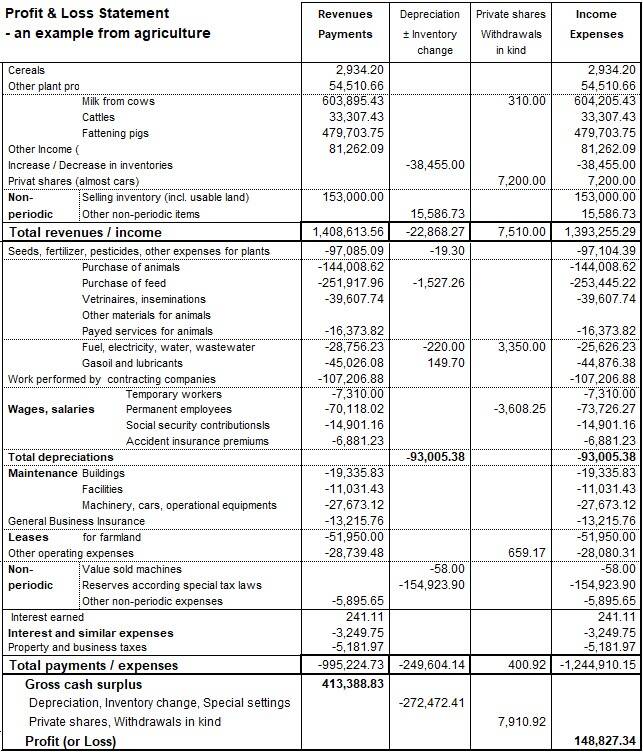

To aid understanding, it is helpful if accountants present their P&L in the following format, which is used in agriculture. It starts with the revenues and payments column. This column ends with the gross cash surplus. After inventory changes, depreciation and some private supplements, the income and expenses column ends with the profit. The following diagram shows the results of a farm in Germany.

This farm employs five full-time laborers and has a depreciation value of over 93,000 euros. Relatively speaking, that's quite a lot.

In the examined year, land where other people wanted to build a house was sold for 150,000 euros. Of course, this is an extraordinary amount of cash. As noted in column 2, German law permits such revenue to be hidden for reinvestment in land or buildings within about two years.

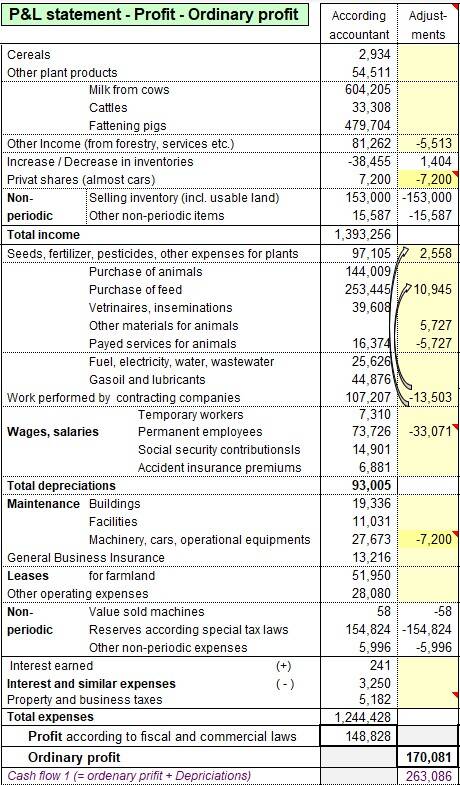

It is up to the analyst to carry out further work. In principle, the necessary adjustments are easy to make in a table like the one shown. The real problem is knowing which adjustments are needed. For instance, in a family business, the son of the owners may receive wages that the accountant records in the books. However, from an economic viewpoint, we need to know how much ordinary profit is left for the entire family. As shown in the following figure, €33,071 of wages are deducted and transferred to private (personal) withdrawals.

The accountant's office must provide a reliable, detailed basis. However, cash flows and similar matters are not their area of expertise!

The adjustment column can also be used for reallocations. This column ends up with the 'ordinary profit'. Please note that in this presentation, the signs for expenses have been changed from minus to plus for easier reading. This table (out of the program JUP PS) shows even the cash flow 1 (operational cash flow). For this, the well-known formula used by practitioners is employed:

Operational cash flow = ordinary profit + depreciation

As has always been the case with operational cash flow, interest on debts is deducted.

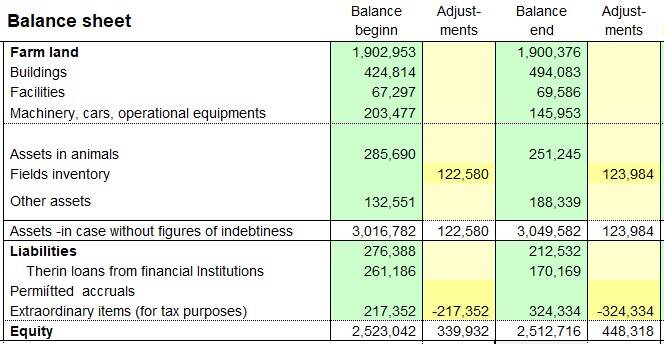

Assets, debts and equity

It is usually referred to as the balance sheet, or simply the balance. The formula is:

Equity = Total Assets - Total Liabilities

Accountants' balance sheets can also be transferred to analysts' balance sheets using adjustments according to economic rules.

Only a few adjustments were made to the balance sheet here. In Germany, there is an option to value the field inventory or not. However, economically, the field inventory has value, at least by the middle of the year (this is the balance sheet date for agriculture in Germany). Therefore, the analyst can add assets of around 123,000 euros for field inventory.

In the JUP PS programme, it is proposed that the entire amount be neutralised for extraordinary items (see last lines).

In the farm example shown the economic balance sheet more equity (at the end of the year plus €448.318). Often, the opposite is true, due to an overvaluation of real assets.

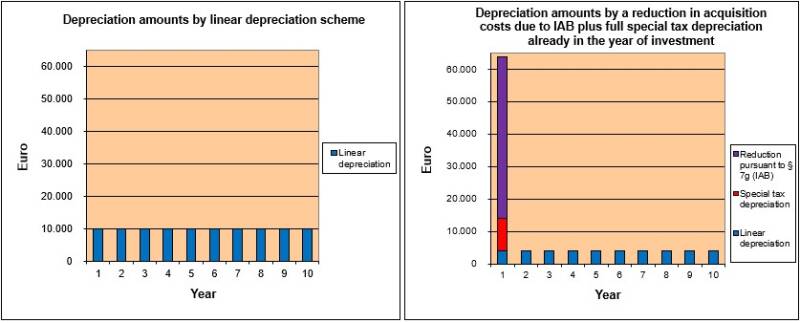

Depreciation can legally be manipulated - and that way the profit, too !

In economic business management, depreciation is usually calculated in a linear manner. However, according to tax rules, depreciation can generally be legally manipulated. For political reasons, it is often permitted to choose a 'degressive' kind of depreciation. Furthermore, a reduction in acquisition costs may be permitted (e.g. for small companies). Companies may even legally transfer depreciation to the period before the time of investment. However, in such a case, depreciation in later years is much reduced, meaning that the later profit is artificially higher than it would be with linear depreciation!

Indeed, entrepreneurs should not claim depreciation in advance if prices or yields were poor in a given year. The author knew several tax consultants who advised claiming IAB (depreciation in advance in Germany), even when hardly any profit was achieved — it's crazy, isn't it?

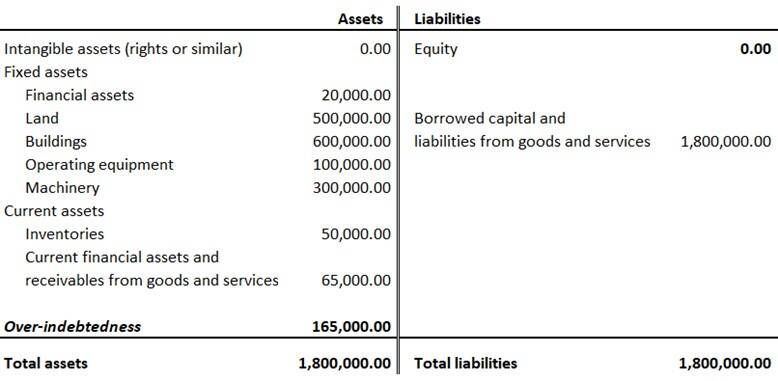

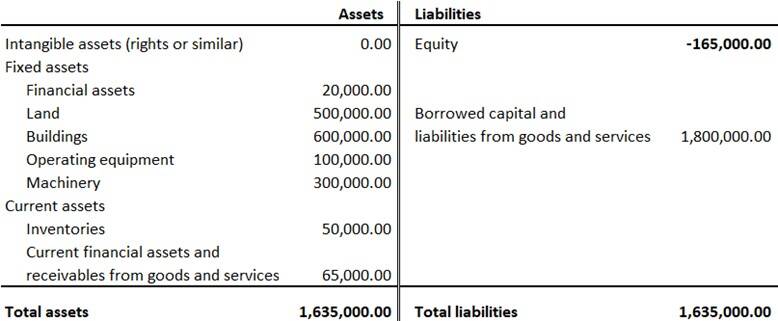

Assets and equity in an over-indebted business

The convention of 'debit and credit' was invented during the era of mental arithmetic and first written down by Luca Pacioli in 1494. According to this convention, a negative number must never appear in a column of numbers. This convention is also applied to balance sheets, where equity must not have a value of less than zero. Below are two tables for demonstration purposes.

To achieve a balance in an over-indebted company, you have to add the amount of debt that is not covered by assets to the assets side! This means that additional assets are created artificially.

Now, (1,000digital arithmetic has been in use, since the 1960s. Since then, a negative equity figure can be shown.

According to the "plus and minus" logic, the total assets are less than the total debts (€1,880,000). This logic must replace the convention of "debit and credit". Furthermore, the national laws must recognise the consequences of digitalisation.

Accountants do not think like entrepreneurs

When discussing, we should realize that accountants and entrepreneurs (as well as analysts) have different manner of thinking. The following diagram may illustrate this.

It is astonishing that some analysts and consultants are willing to follow the 'standards' of a board of accountants, like IHRS 18. Surely, you will never find a real accountant who replaced an entrepreneur. The opposite may happen if a person fails as an entrepreneur.