Double-entry accounting - Let's recognice the digitalisation

Why was this page written?

The author learnt accounting at school using the 'debit and credit' convention. After starting to teach in 1982, he developed 'double-entry tables' that did not use the 'debit and credit' convention. His students and master of agriculture candidates proved that it works with 'plus and minus' alone.

Unlock the power of double-entry accounting, moving beyond the traditional concepts of 'debit' and 'credit'. Discover a modern approach designed for today's business world that focuses on what truly matters for achieving financial clarity and effective management.

In 1494, when Luca Pacioli described the bookkeeping principle, only mental arithmetic was possible. With mental arithmetic, almost everyone can only add a column of numbers if all the figures have the same sign — the "plus". Thus, a system had to be invented in that era with only one sign in each column. The mental math was the real reason for the "debit and credit" convention, and nothing else !

Since the 1960s, everyone is making digital mathematical additions. In German law, the P&L statement has changed to the scaggered form, with plus or minus in the colums. However, when it comes to the balance sheet, the convention from 1494 is still used in law.

Many business management and administration experts were still unaware of digitalisation! Therefore, both the new method and the traditional convention are described in detail. For this, see the file 'Business Management: Basics, Indicators, Examples' (Chapter 9).

Double-entry accounting without 'Debit and Credit' offers a realistic approach.

It saves teaching time, as the author's simplified method makes it quicker to grasp accounting principles. It eliminates illogical complexities. The system also avoids inconsistencies in the case of a company that is over-indebted (see the website page on assets and equity for more information). By removing outdated jargon, accounting becomes more logical. The 'plus and minus' logic is also sufficient in accounting theory.

The headings show the four classes of accounts:

. Financial accounts and real asset accounts,

. Profit and loss accounts, and private (personal) accounts.

Every entry must be made twice. After every entry, the two checksums below (in the fourth-to-last line) must be equal. If they are, then your doubling has been done correctly, at least formally.

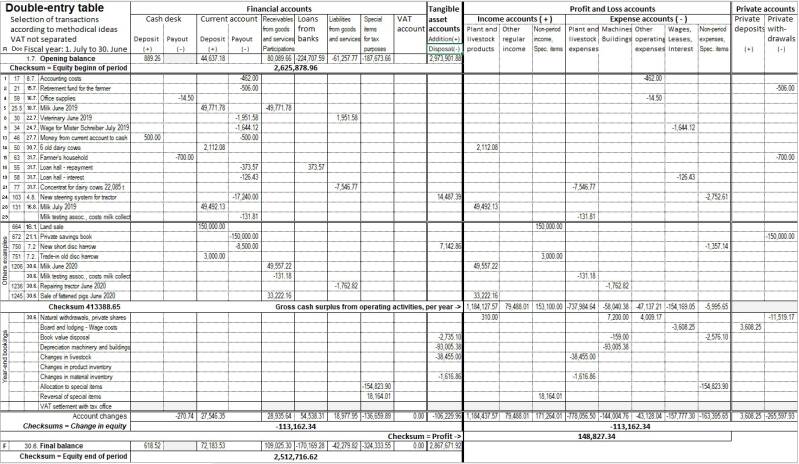

The following 'double-entry table' (shown for a whole year, but shortened) proves that accounting theory can be understood without using the terms 'debit' and 'credit'. However, you must pay close attention to the mathematical signs. Put simply, if the doubling is beyond the thick black line in the middle, then the sign changes (see, for example, the entry 'Board and lodge - wage costs', where private living expenses are transferred to the company's expenses). If the doubling is between the same blocks, then the sign remains the same (the so-called active or passive exchange).

At the end of the year, this double-entry table even shows the profit or loss. Digital addition makes double-entry much easier.

For a more detailed discussion, see the following papers:

. 'Business Management: Basics, Indicators, Examples' (Chapter 9) and

. 'Finally Digital: Double-Entry Bookkeeping Without 'Debit and Credit'.

The latter article contains a long list of references.

You can download the Excel table 'i Double-entry Table Digital Logic'.

This allows you to test the table yourself.